{kind=link}

It’s time for an additional mortgage match-up of us. At present, we’ll have a look at 10-year mortgages versus the 30-year fastened mortgage to see how these residence loans stack up in opposition to each other.

My guess is the extra 30-year fastened mortgage charges rise, the extra customers can be wanting into different mortgage merchandise like these.

However earlier than we get began, it’s essential to notice that there are two very various kinds of 10-year mortgages on the market.

One is a fixed-rate mortgage that’s paid off in only a decade, and the opposite is an adjustable-rate mortgage, which takes three full a long time to repay.

So clearly it’s worthwhile to pay actual shut consideration right here to make sure you know what you’re getting your self into.

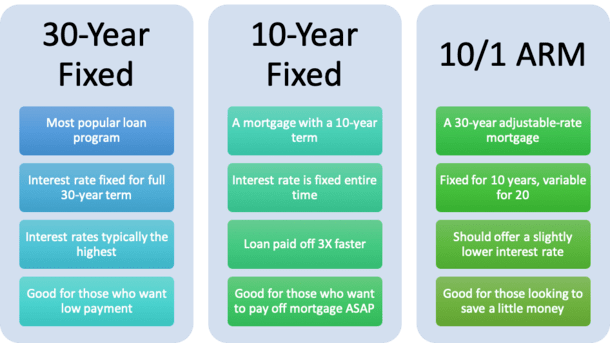

Two Very Totally different Forms of 10-12 months Mortgages

- There are two sorts of 10-year mortgages accessible to owners at this time

- The ten/1 ARM (it’s fastened for the primary 10 years and adjustable for the remaining 20 years of the mortgage time period)

- And the 10-year fixed-rate mortgage (it includes a fastened rate of interest for all the 10-year mortgage time period)

- Ensure you already know what you’re really getting when evaluating mortgage applications

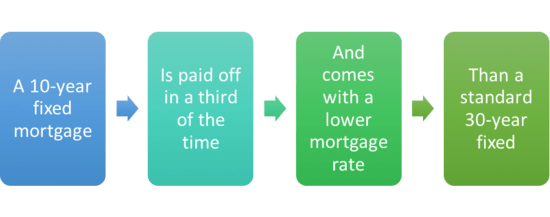

There are 10-year fastened mortgages, which have a mortgage time period of 10 years. Yep, only a decade and they’re paid off in full.

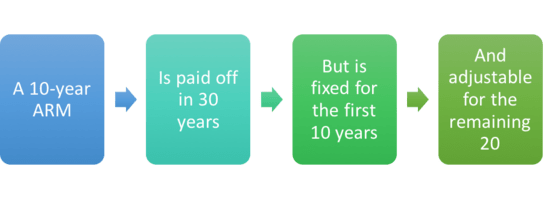

Then there are 10-year adjustable-rate mortgages, which have a time period of 30 years. Big distinction for various causes.

The primary kind of mortgage is fairly simple. It’s much like a 30-year or 15-year fastened mortgage, solely shorter. As talked about, the mortgage period is simply 10 years.

What this implies, should you occur to be courageous sufficient to go together with this mortgage program, is that your month-to-month mortgage fee can be fairly excessive because you solely get 120 months to pay it off.

In spite of everything, should you solely get 10 years to repay your whole mortgage steadiness, versus 30, you’ll must give you some sizable month-to-month funds to get it right down to zero in a rush.

As such, this mortgage kind isn’t for the faint of coronary heart, neither is it for the borrower with no cash of their financial savings account.

Nevertheless, 10-year loans will prevent a ton of cash in curiosity. And that’s precisely why somebody would select this sort of mortgage. To save lots of a lot of cash!

When you don’t consider me, seize a mortgage calculator and decrease the time period from 360 months right down to 120 months. You’ll be amazed. That doesn’t imply it’s a no brainer, as I identified in my prepay the mortgage or make investments article.

And most folk in all probability can’t even afford such excessive funds, or just don’t need to pay down their mortgage that aggressively.

So this sort of residence mortgage received’t be an possibility for the borrower with a low down fee, nor will it possible swimsuit a first-time residence purchaser.

For instance, FHA loans and VA mortgages in all probability don’t come on this taste, however it’ll possible be an possibility for a jumbo mortgage.

The “different” 10-year mortgage you’ll see out there may be the “10/1 ARM,” which is fastened for the primary 10 years, and yearly adjustable for the remaining 20. Merely put, it’s a 30-year mortgage with an preliminary 10-year fastened interval.

This makes it a hybrid ARM due to its fastened/adjustable nature. It additionally means the month-to-month funds have the flexibility to regulate each increased and decrease as soon as these first 10 years are up.

We’re principally speaking about two mortgage merchandise on reverse ends of the spectrum.

One which pays down all the residence mortgage steadiness in a 3rd of the time (sometimes it takes 30 years), and one which’s an ARM, which some think about higher-risk than conventional fastened mortgages.

So, are both mortgage applications a more sensible choice than the traditional 30-year fastened mortgage when shopping for actual property? Let’s see.

10-12 months Fastened Mortgages Solely Final Ten Years

- A ten-year fastened mortgage solely lasts for a decade

- It’s paid off in full in that point however month-to-month funds are very excessive

- You solely get a 3rd of the standard time to repay you residence mortgage

- Whereas funds are steep, it can save you a ton of cash and be free and clear very quickly!

When you’re actually, actually critical about paying off your mortgage quick, the 10-year fastened may very well be the mortgage for you. You’ll acquire residence fairness hand over fist very quickly in any respect.

Simply notice that your mortgage fee can be big relative to different, extra conventional choices that offer you extra time to repay your steadiness.

When you’ve got scholar loans and bank card debt, you might need to go together with one thing a little bit extra conservative. So use an affordability calculator first to find out should you can qualify, not to mention deal with the funds.

For instance, on a $250,000 mortgage quantity, a 10-year fastened mortgage with an rate of interest of three% would include a month-to-month mortgage fee of $2,414.02.

Examine that to a month-to-month fee of $1,787.21 on a 15-year fastened at 3.5%, and a fee of $1,193.54 on a 30-year fastened at 4%. It’s about double the 30-year fee.

Discover how I even factored within the decrease mortgage price afforded to the 10-year fastened and 15-year fastened and the fee continues to be considerably increased.

Nicely, whereas the fee on the 10-year fastened is sort of a bit increased, you’d solely pay about $40,000 in curiosity over these 10 years of mortgage compensation.

On the 15-year fastened, you’d pay about $72,000 in curiosity, and on the 30-year fastened you’d pay almost $180,000 in whole curiosity. Sure, you learn that proper. Practically 5 instances the quantity of curiosity versus the 10-year mortgage!

This illustrates why somebody would go for the shorter time period 10-year fastened. A decrease mortgage price and far much less curiosity paid.

And a house bought with one among these loans can be free and clear far more rapidly, if that’s your objective or you’re near retirement.

Talking of, it may very well be a good selection for the home-owner who obtained a late begin, as a way of taking part in catch-up.

Nevertheless it solely is sensible should you actually need to repay your mortgage quick, and have the means to do it with out breaking the financial institution.

10-12 months Fastened Mortgage Charges Are Decrease

- One other benefit of a 10-year fastened is the decrease rate of interest

- They’re cheaper than 15-year and 30-year fastened mortgages

- How less expensive could depend upon the financial institution/lender in query

- Maybe .25% decrease than a 15-year fastened and .75-1% decrease than a 30-year fastened

Talking of rates of interest, let’s discuss what you would possibly count on to obtain on a 10-year fastened mortgage.

First, not all lenders provide this system. It’s considerably of a specialty mortgage program, so you should definitely ask about it particularly when chatting with a mortgage officer or search it out straight when evaluating present mortgage charges.

It’s actually not as widespread as a 30-year or 15-year fastened. So when you discover a lender that does provide the mortgage, you would possibly see that 10-year mortgage charges are an .125 (eighth) higher than a comparable 15-year fastened. Possibly 1 / 4 decrease…

In different phrases, if the 15-year fastened is priced at 3.25%, the 10-year fastened mortgage price may be provided at 3.125% or 3%. It’s not going to be an enormous distinction.

Some mortgage lenders could not even worth the 2 sorts of loans in another way. The one distinction may be decrease closing prices on the 10-year fastened.

In the meantime, the same 30-year fastened would possibly go for 3.875%, so that you’re taking a look at a couple of .75% low cost, kind of. That’s fairly important.

Tip: The distinction between a 15-year fastened mortgage charges and 10-year fastened mortgage charges could also be marginal and even nil.

So taking the long term on the 15-year fastened might offer you some a lot wanted respiratory room. You possibly can all the time make bigger funds every month to pay it down faster.

10-12 months Fastened Mortgage Professionals and Cons

The Good

- Repay your mortgage in simply 10 years!

- Get a decrease rate of interest than a 15-year or 30-year fastened

- Pay a lot much less curiosity over the shorter mortgage time period

- Extra of your month-to-month fee goes towards principal steadiness

- Personal your own home a lot quicker

- Might be a good selection for a house purchaser who obtained a late begin

The Unhealthy

- Month-to-month funds can be a lot increased

- Could not qualify for an costly residence

- Could restrict your buying energy

- Might get into fee bother in case your revenue drops

- Your cash may be higher served elsewhere

10-12 months ARMs Are a Totally different Beast

- A ten-year ARM is an adjustable-rate mortgage

- It’s fastened for the primary 10 years and adjustable for 20 years

- It has a 30-year mortgage time period similar to a 30-year fastened

- However is topic to annual price changes after the primary 10 years

Right here’s the place issues can get complicated, and even deceptive. Some mortgage firms promote 10-year ARMs as in the event that they’re fastened mortgages, which simply isn’t the case. Or at greatest half the story.

They principally use that preliminary 10-year fastened interval to their benefit when placing collectively advertising supplies. However they’re not 10-year loans. They’re 30-year loans, finish of story.

In fact, mortgage lenders could make 10-year ARMs seem actually engaging by touting the decrease rate of interest that accompanies them.

In spite of everything, an ARM will just about all the time be priced decrease than a 30-year fastened mortgage as a result of they are going to finally develop into adjustable.

So you may see why a buyer might imagine the 10-year ARM is the higher selection palms down.

However the reality of the matter is that these loans are nonetheless adjustable-rate mortgages in fixed-rate clothes.

And when it comes right down to it, they often aren’t that less expensive than a standard 30-year fastened as a result of they’re fastened for a full decade.

10/1 ARM Charges Could Come at a Slight Low cost

- Whereas rates of interest will range over time and by mortgage lender

- Count on a ten/1 ARM to cost barely under a comparable 30-year fastened

- Maybe simply .125% to .25% cheaper in price relying on the corporate

- The low cost is marginal as a result of 10 years continues to be a very long time to supply a set rate of interest earlier than the primary adjustment

Now let’s talk about 10/1 ARM charges, which usually come cheaper than 30-year fastened charges.

Nevertheless, the rate of interest could solely be .125% or .25% cheaper since you get a set price for a full decade earlier than any adjustment takes place.

Many of us don’t even keep in the identical residence or hold their mortgages for a decade, so the ten/1 ARM might make sense and prevent some dough with little to no draw back.

Nevertheless, this additionally explains the shortage of a giant low cost relative to the 30-year fastened.

When you’re not comfy with a mortgage program that options adjustable charges, steer clear. The financial savings might not be definitely worth the stress.

Assuming you intend to maneuver inside 10 years (or refinance your mortgage for some purpose), going with a 10-year ARM ought to offer you a reduced fastened price for a big time frame whilst you determine issues out.

In fact, if you already know you received’t keep even 5 years, it may very well be even smarter to look to the 5/1 ARM as a substitute, which is able to include a fair decrease rate of interest.

10/1 ARM Professionals and Cons

The Good

- Decrease rate of interest than a 30-year fastened

- Lengthy fixed-rate interval (120 months)

- Most owners transfer or refinance in a decade’s time anyway

- So you might by no means need to face an rate of interest adjustment

The Unhealthy

- The rate of interest might not be less expensive than a 30-year fastened

- Price can alter increased after 10 brief years

- Might face fee issue if charges alter considerably increased

- Or be pressured to refinance at unfavorable phrases if charges rise throughout that point

In abstract, pay shut consideration to those very totally different mortgage varieties so you already know which kind of 10-year mortgage you’re really getting…

Learn extra: 30-year vs. ARM