{kind=link}

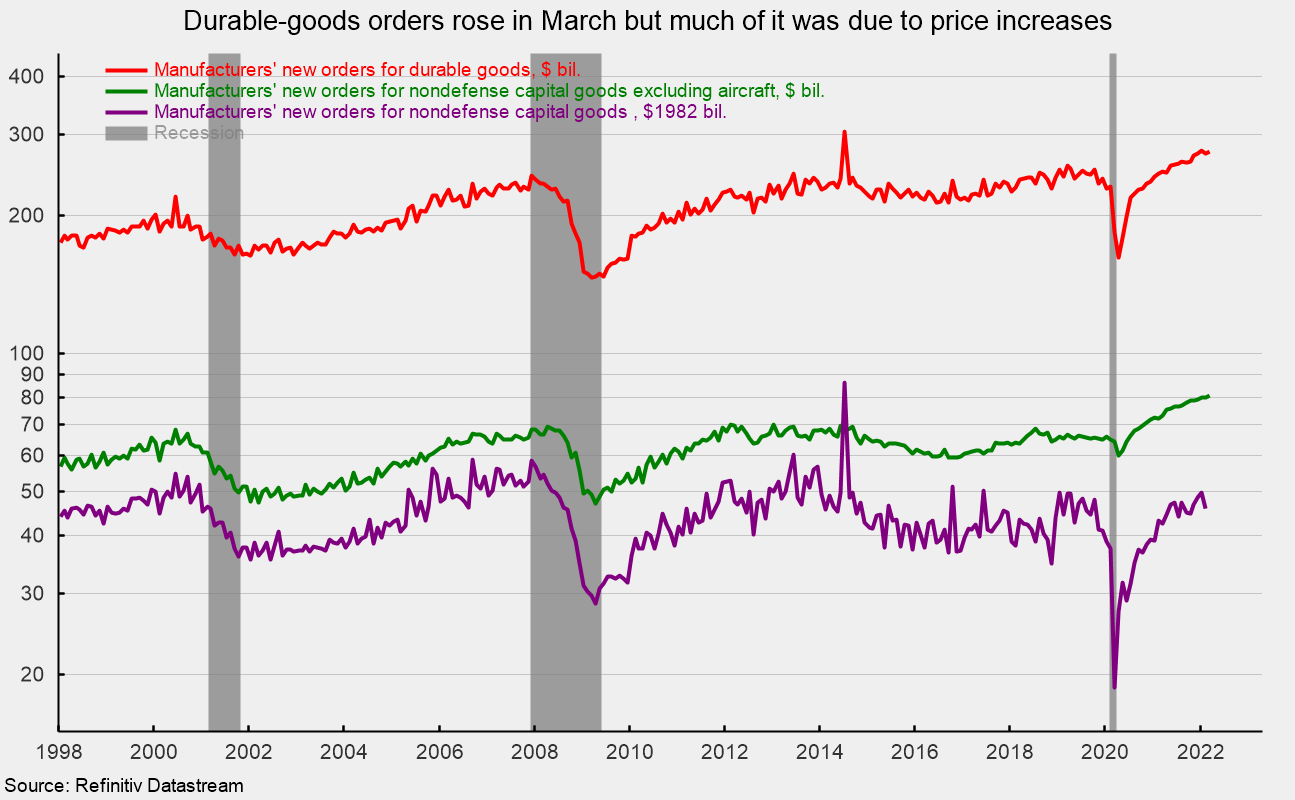

New orders for sturdy items elevated 0.8 p.c in March, rebounding from a 1.7 p.c drop in February. Complete durable-goods orders are up 11.9 p.c from a yr in the past. The March acquire places the extent of whole durable-goods orders at $275.0 billion, the third highest on file (see first chart).

New orders for nondefense capital items excluding plane, or core capital items, a proxy for enterprise gear funding, jumped 1.0 p.c in March after falling 0.3 p.c in February. Orders had risen for 11 consecutive months from March 2021 via January 2022 and have elevated 21 of the final 23 months since April 2020. The outcomes put the extent at $80.8 billion, a brand new file excessive (see first chart).

Nevertheless, accelerating value will increase have an effect on capital items. In actual phrases, after adjusting for inflation, new orders for nondefense capital items have been $45.9 billion in February, measured in 1982 {dollars}, a excessive stage by historic comparability however properly shy of the file excessive (see first chart). Producer costs for client sturdy items rose 0.7 p.c in March whereas producer costs for capital gear rose 0.8 p.c, suggesting that in actual phrases, new orders for sturdy items have been roughly flat whereas actual new orders for nondefense capital items excluding plane rose a modest 0.2 p.c.

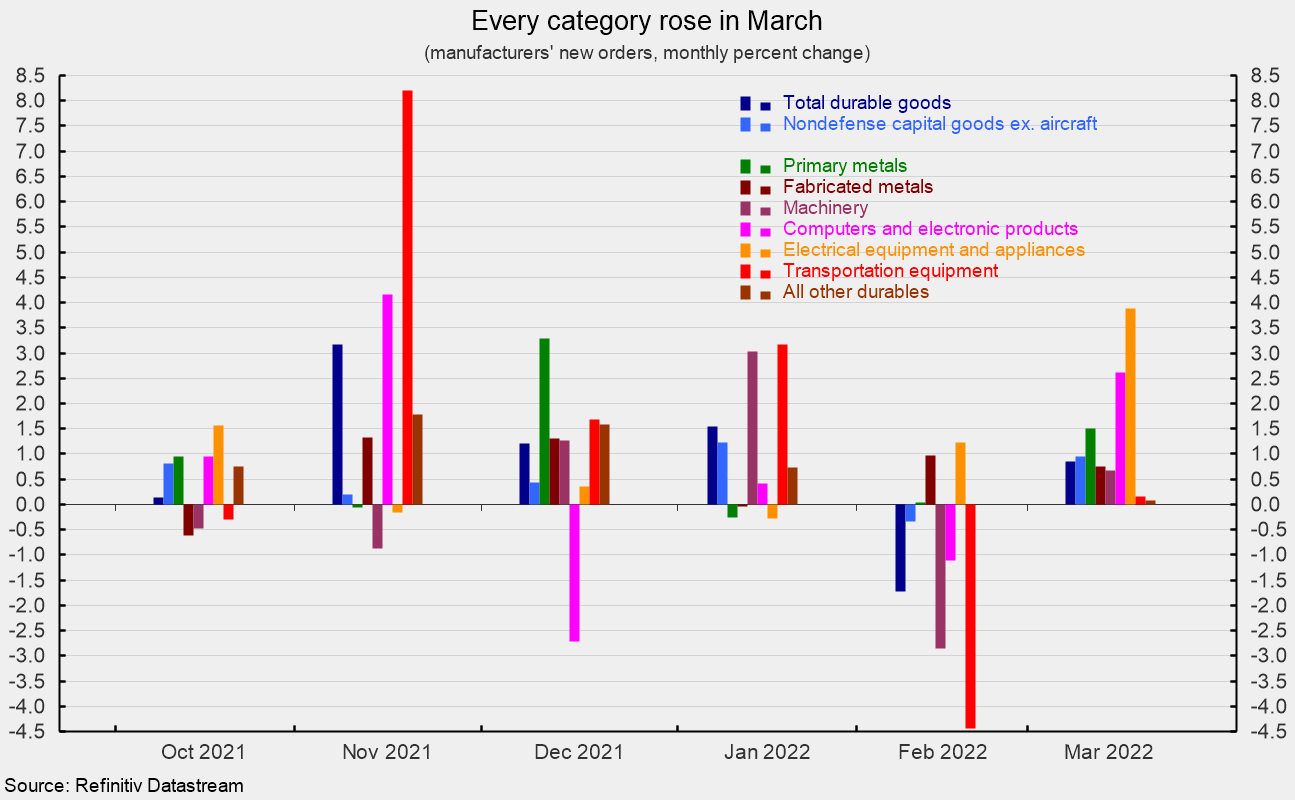

Each class within the durable-goods report confirmed a acquire in March. Among the many particular person classes, electrical gear and home equipment led with a 3.9 p.c enhance, adopted by computer systems and digital merchandise with a 2.6 p.c rise, main metals with a 1.5 p.c acquire, fabricated steel merchandise, up 0.8 p.c, and equipment orders, up 0.7 p.c. Transportation gear added 0.2 p.c with motor automobiles and elements up 5.0 p.c, however nondefense plane was down 9.9 p.c, and protection plane plunged 25.6 p.c (see second chart). From a yr in the past, each main class reveals a acquire.

Sturdy-goods orders proceed to be robust, significantly the core-capital items parts, although a few of the acquire in nominal-dollar orders is because of value will increase. Demand stays strong for the manufacturing sector, and the tight labor market creates incentives to substitute capital for labor. The pandemic could have accelerated structural adjustments to the economic system, affecting labor, housing, manufacturing, and providers.

Nevertheless, the outlook stays unsure. Sustained upward stress on costs continues with demand outpacing provide. Labor and supplies shortages proceed to hamper manufacturing and the Russian invasion of Ukraine has unleashed a wave of volatility and disruptions to the worldwide economic system. Moreover, the Federal Reserve has begun an rate of interest tightening cycle boosting the chance of a coverage mistake. Warning is warranted.

Robert Hughes

Robert Hughes joined AIER in 2013 following greater than 25 years in financial and monetary markets analysis on Wall Road. Bob was previously the top of International Fairness Technique for Brown Brothers Harriman, the place he developed fairness funding technique combining top-down macro evaluation with bottom-up fundamentals.

Previous to BBH, Bob was a Senior Fairness Strategist for State Road International Markets, Senior Financial Strategist with Prudential Fairness Group and Senior Economist and Monetary Markets Analyst for Citicorp Funding Providers. Bob has a MA in economics from Fordham College and a BS in enterprise from Lehigh College.