{kind=link}

- Lively MFs have larger charges in comparison with index funds.

- Lively MF efficiency lags the index over the long run. The SPIVA experiences present that 8 out of 10 Fairness Mutual Funds underperform the US Fairness Index benchmarks when the remark window is stretched out to a 10-year interval. For the yr 2021, 8 out of 10 actively managed fairness funds underperformed the US index.

- Particular person fund success doesn’t final. A tutorial analysis paper by Prof. James Choi and his graduate scholar, Kevin Zhao, “Did Mutual Fund Return Persistence Persist?” (2020) finds that “important efficiency persistence doesn’t exist within the 1994-2018 interval.” Additionally, this NY Instances article for a fast learn.

- Poor tax administration is frequent: Annual taxable distributions and dividends by actively managed MF are important. For these with MF funding property in taxable brokerage accounts, taxes on distributions are a big drag on efficiency. Michael Lane, Head of iShares U.S. Wealth Advisory, experiences:

for the ten years ending in 2019, taxes on distributions diminished returns on the typical annual efficiency of actively managed U.S. Giant Cap Mix mutual funds by 1.79 proportion factors. Over the identical interval, the typical expense ratio of that class was 0.89%. In different phrases, whereas buyers are more and more centered on fund charges – as they need to be – the typical affect of taxes has been almost double that of the expense ratio. (“Don’t let taxes drag you down,” BlackRock Advisor Middle, 5/26/21)

- Alternative Value: Whereas durations of outperformance don’t final, durations of great underperformance are frequent and final for lengthy. Overlooking this chance price requires a sure stage of religion within the funding supervisor.

(Once I learn David Snowball’s commentaries of chosen funds, I can see his significant conversations with sure fund managers have allowed area for his religion to develop. That is maybe an vital purpose for energetic MF managers to make themselves extra obtainable.) - Lively bond funds didn’t shield in down markets: I owned loads of energetic bond managers. Low-interest charges for a decade seduced me to speculate with them. Their supply of upper carry was largely pushed by credit score danger and illiquidity. For some purpose, I anticipated them to skirt an fairness market crash. When in March 2020, I noticed my bond funds down 15-20%, I used to be dissatisfied. I didn’t promote out of these funds into shares as I hoped to. Realizing I used to be the better idiot to count on a free lunch, I finally exited these energetic bond funds. (Within the 2022 market sell-off, the energetic bond funds appear to be predictably struggling. There’s little outperformance adjusted for the period.)

- Stream of Funds and the Sage of Omaha’s future widow’s portfolio: The sum of money flowing into passive investing from energetic over the past ten years should be a couple of trillion {dollars}. Warren Buffett has stated that when he dies, he would really like his widow’s property to be invested 90% within the S&P 500 Index and 10% in T-Payments. Cumulatively, the excessive charges and underperformance of most actively managed fairness MF have been fairly clear for all to see.

None of that is to say that energetic fund administration doesn’t work; solely that I couldn’t make it work for me. Others might need a distinct and extra promising story. My aversion to energetic MF investing makes me an odd bedfellow within the Mutual Fund Observer neighborhood. But it surely additionally permits me a possibility to study from others who’ve religion.

Affirmation Bias

Peter Lynch’s contradictory feedback about my biases and analysis got here unannounced and compelled me to assume: “What’s his incentive to name the passive crowd unsuitable?” I questioned. “Is that this an advisor to Constancy speaking or is there real benefit in his argument?”

I peered inside my very own thoughts. By ignoring Mr. Lynch’s message and searching just for analysis that supported my present bias and thesis, I might be participating within the behavioral shortfall generally known as Affirmation Bias.

Right here is Daniel Kahneman, creator of Pondering Quick and Sluggish, as quoted in an article by Drake Bear in The Lower: “The place does affirmation bias come from? Affirmation bias comes from when you’ve gotten an interpretation, and also you undertake it, after which, top-down, you pressure the whole lot to suit that interpretation.”

Affirmation Bias makes us hunt down like-minded folks, who share our opinions, our views on the world, and on investments. Affirmation Bias means I search for and down for info that can make me really feel higher about my already established funding thesis. It means overlooking each contradictory truth as a result of it will be inconvenient to my mind-set. All buyers are prone to Affirmation Bias as a result of there’s a fantastic line between deeply believing one thing and questioning that perception by placing it to the take a look at. Most individuals discover it troublesome to study and make investments properly.

For instance, there are believers and non-believers in cryptocurrency. Whichever aspect one is influenced by, that’s the “right” aspect. Each dialogue has the texture of pushing folks deeper into their established biases.

Exactly, subsequently, within the subject of investing, speaking to individuals who see issues dramatically otherwise from us can typically deliver us the best profit. It may possibly save us from our biases and self-selected group assume. To keep away from Affirmation Bias, if I’m really bullish on a inventory or an funding thought, I discover the most important bear and take heed to his/her arguments.

I’ve learnt that I normally study from these conversations and mood my bullish or bearish enthusiasm. And on uncommon events, I’ve strengthened my very own convictions and guess greater, as a result of I do know the alternative thesis is weaker.

I’ll admit that it’s onerous to bear this ego-crushing train. It’s far simpler to dam out the opposite voice. It’s so way more snug to simply see my model of the world as right and each different model unsuitable.

Taking President George W. Bush’s “You’re both with us, or in opposition to us” may match in geopolitics, however it’s a catastrophe recipe for an investor. Being open-minded is extra profitable.

As inconvenient because it was, I knew that Mr. Lynch was a legend, his phrases had been counter to the music in my very own head, and that I must go discover out if he was right. I would change my thoughts and study one thing.

The Evaluation

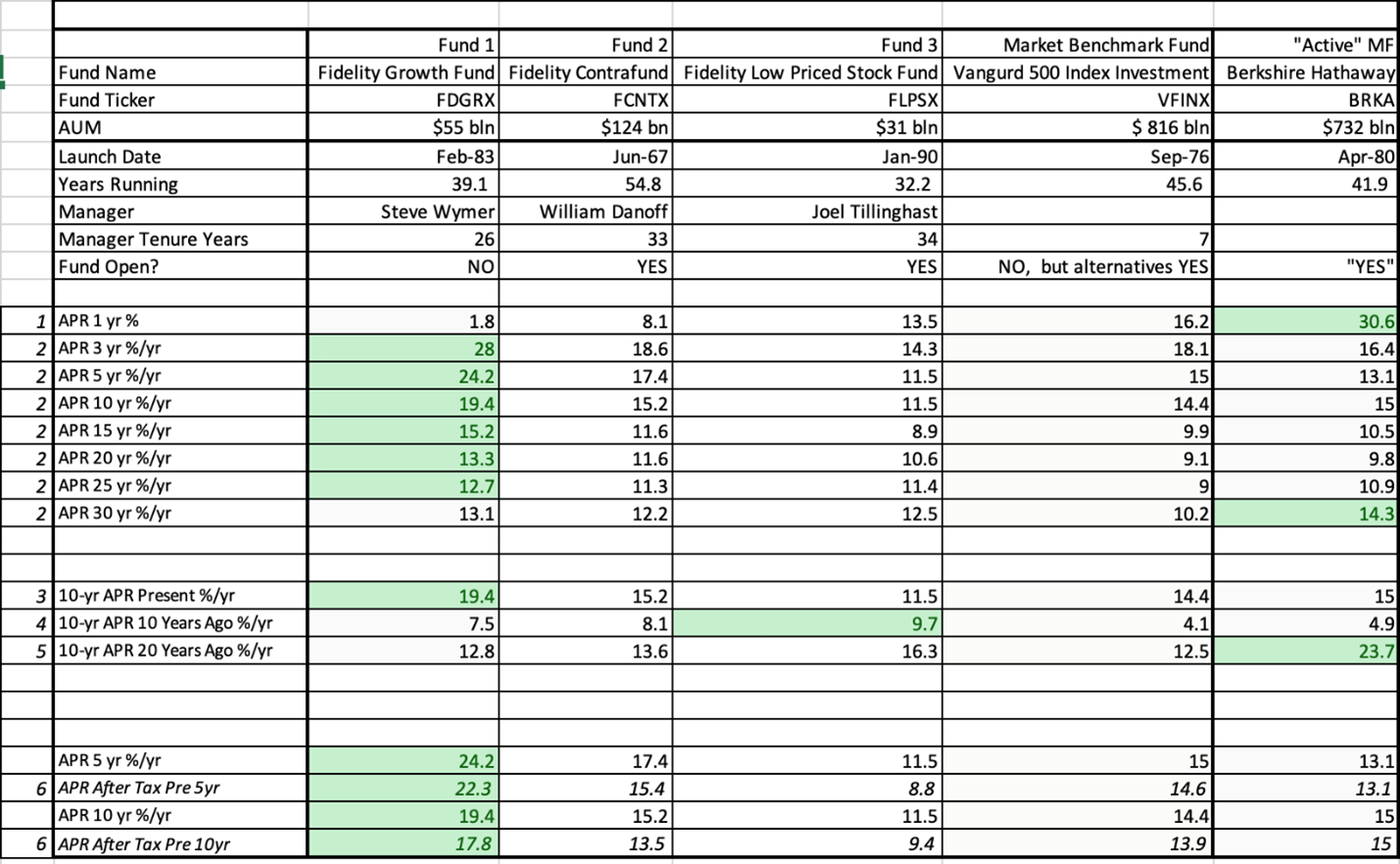

Utilizing the MFO Premium search engine, I analyzed the three aforementioned Constancy funds. For good measure, I added the Vanguard 500 Index Fund, and likewise Berkshire Hathaway A shares (my proxy for a well-run actively managed funding). The detailed outcomes desk is highlighted on the finish of the article together with some technical explanations. Here’s a fast evaluation:

-

- The Constancy Progress Firm: Mr. Lynch was right. This fund has completely crushed the market benchmark and even Berkshire Hathaway over the past 20-30 years. Sadly, the Fund is closed to New Buyers as of April 2006.

- The Constancy Low Inventory Fund: This fund did very properly within the 90s however NOT since then. It’s not one of many funds which have beat the market over the past 10 and 20 years. Mr. Lynch was unsuitable right here.

- The Constancy ContraFund: Combined outcomes.

-

- The fund is Open and has usually crushed the Market Indices.

- This outperformance has been pushed by important energetic motion throughout the portfolio.

- The distributions from the energetic buying and selling have tax penalties.

- Adjusted for taxes, the fund’s outperformance has disappeared in opposition to the market.

- This energetic fund may work for tax-deferred accounts.

-

- Berkshire Hathaway: Many buyers are essential of Warren Buffett for not paying a dividend or distribution. However because of NOT paying a distribution, adjusted for taxes, this inventory has began outperforming. This, regardless of the widely famous lack of ability of Berkshire to make use of its giant money pile for appropriate elephant investments.

Conclusion

Have I answered the query I began with on energetic vs passive? Has the evaluation affirmed my present biases or made me change my opinion about something?

-

- The Constancy Progress Firm’s large outperformance is an efficient wake-up name for me. I learnt that very good and constant outperformance exists in a Mutual Fund, even in at present’s benchmark-driven passive market.

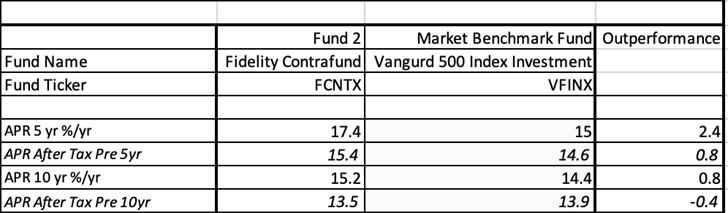

- The Contrafund is fascinating as a result of it each outperforms and underperforms the market benchmark fund on the identical time. Its outperformance is from Danoff’s funding acumen, and the underperformance from the excessive taxes on distribution the fund pays. On a associated be aware, Morningstar simply downgraded Contrafund (3/22/22) in recognition of the large constraints imposed on a supervisor whose technique (which covers Contrafund, clones, and associated accounts) has grown to $250 billion.

- David Snowball had an fascinating tackle the Contrafund. Danoff has educated loads of analysts. How come none of them have carried out as properly exterior of the Contrafund? Perhaps Danoff is Betting on the Contrafund means hoping Danoff sticks round.

- I’m now open to the thought that there’s a choose variety of fund households (Primecap, Constancy, Wasatch, Grandeur Peak to call a couple of) the place the investor has the next shot than the typical actively managed mutual fund. I’m open to studying and studying extra about profitable MF managers so I can kind religion.

- For many of my funding property, I nonetheless really feel snug within the heat blanket of passively managed index funds. Solely after I’ve substantial religion in a fund administration staff would I think about transferring my property, and I might be in no rush to do that.

Keep in mind: be part of the dialog by finishing our fast, straightforward and nameless MFO energetic/passive choice snapshot

For readers who take pleasure in trying on the detailed information behind my arguments, I’ve reproduced the outcomes of a side-by-side comparability of the short- and long-term efficiency of Mr. Lynch’s favourite funds. And since taxes sting, I’ve additionally included their tax-adjusted efficiency. For every metric, the fund with the only highest efficiency is flagged with a inexperienced field.

Detailed efficiency file: three Constancy stars, the S&P 500 and Mr. Buffett

What’s APR: It’s the Annual Share Return of a fund together with the Value and Dividend Return, in addition to the charges paid.

-

- APR 1yr %: Complete fund Return over the past 12 calendar months (March 2021-Feb 2022).

- APR 3yr %/yr.: The whole returns are taken for the final 36-months after which recalculated to kind a median compounded annual return for the interval. This has the impact of averaging the great years with the dangerous years to offer us an approximate quantity the fund delivered to its buyers over the 3-year interval. This identical calculation is completed for the APR 5, 10, 15, 20, 25, 30 within the MFO search engine (or in most monetary web sites).

- 10-yr APR Current %/yr: The fund’s 10-year complete return when annualized on common from Mar-2012 to Feb-2022.

- 10-yr APR 10 Years In the past %/yr: The fund’s 10-year complete return when annualized on common from Mar-2002 to Feb-2012.

- 10-yr APR 20 Years In the past %/yr: The fund’s 10-year complete return when annualized on common from Mar-1992 to Feb-2002.

- APR After Tax Pre 5yr: The fund’s 5yr APR %/yr is adjusted all the way down to account for the taxable distributions made by the fund. The belief is the investor is holding the fund within the taxable account and is taxed on the highest marginal strange earnings tax charge on the federal stage. No tax is subtracted on the State and Native stage.

The After-Tax APR numbers are reported by the funds to the SEC because the early 2000s. This measure was added lately to MFO Premium. Present fund holders of actively managed mutual funds obtain distributions in a tax yr when:-

- A fund’s inventory holdings pay dividends

- A fund liquidates positions with short-term and long-term capital good points

- Different fund holders exit their fund funding and pressure the fund to liquidate positions.

-

-

- Fund holders within the Contrafund have been receiving such distributions and it’s been consuming into their complete returns.