{kind=link}

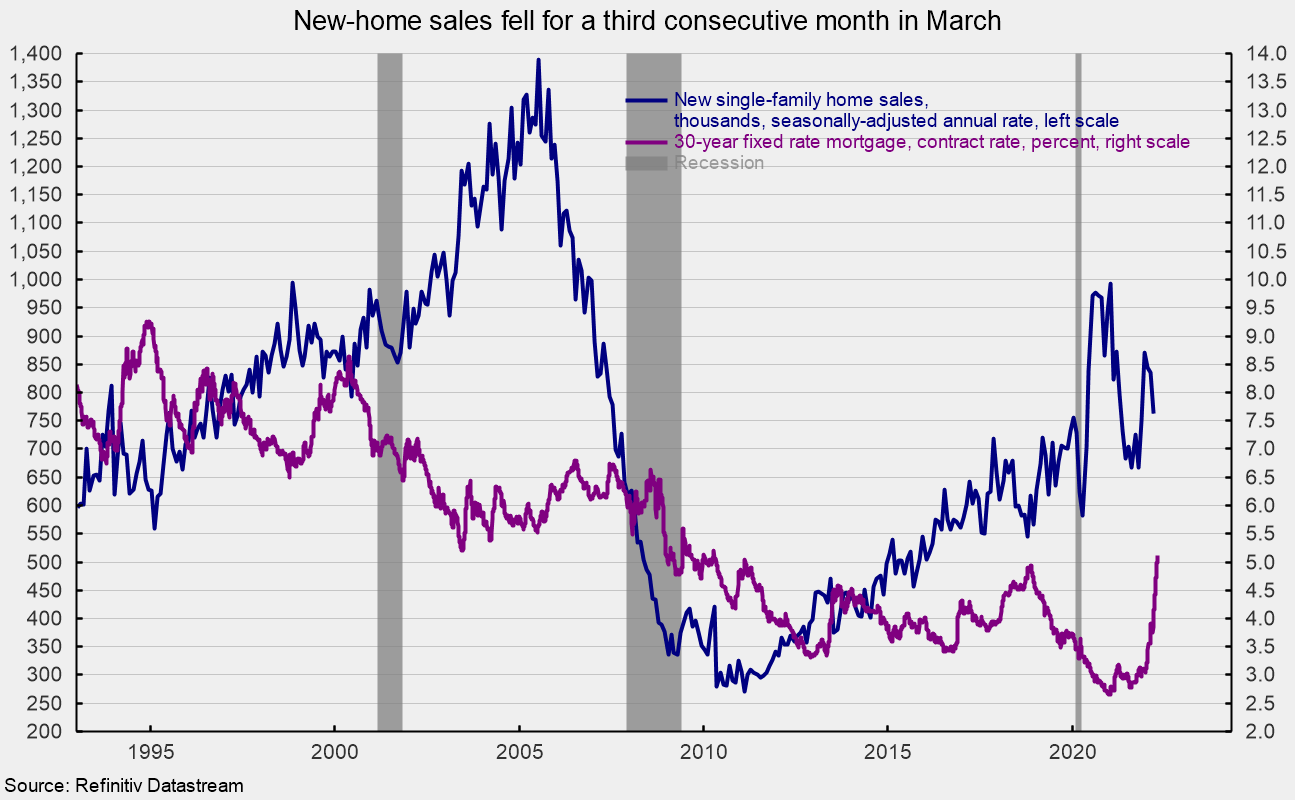

Gross sales of latest single-family houses fell in March, declining 8.6 % to 763,000 at a seasonally-adjusted annual charge from a 835,000 tempo in February. The March drop follows a 1.2 % decline in February and a 3.0 % drop in January. The three-month run of decreases leaves gross sales down 12.6 % from the year-ago stage (see first chart). New residence gross sales surged within the second half of 2020 however then slowed sharply within the first three quarters of 2021, hitting a low of 667,000 in October. Following the October low, gross sales posted two robust positive aspects in November and December however have reversed a few of these positive aspects within the first quarter of 2022 (see first chart). In the meantime, 30-year fastened charge mortgages have been 5.11 % in late April, up sharply from a low of two.77 % in August 2021 (see first chart).

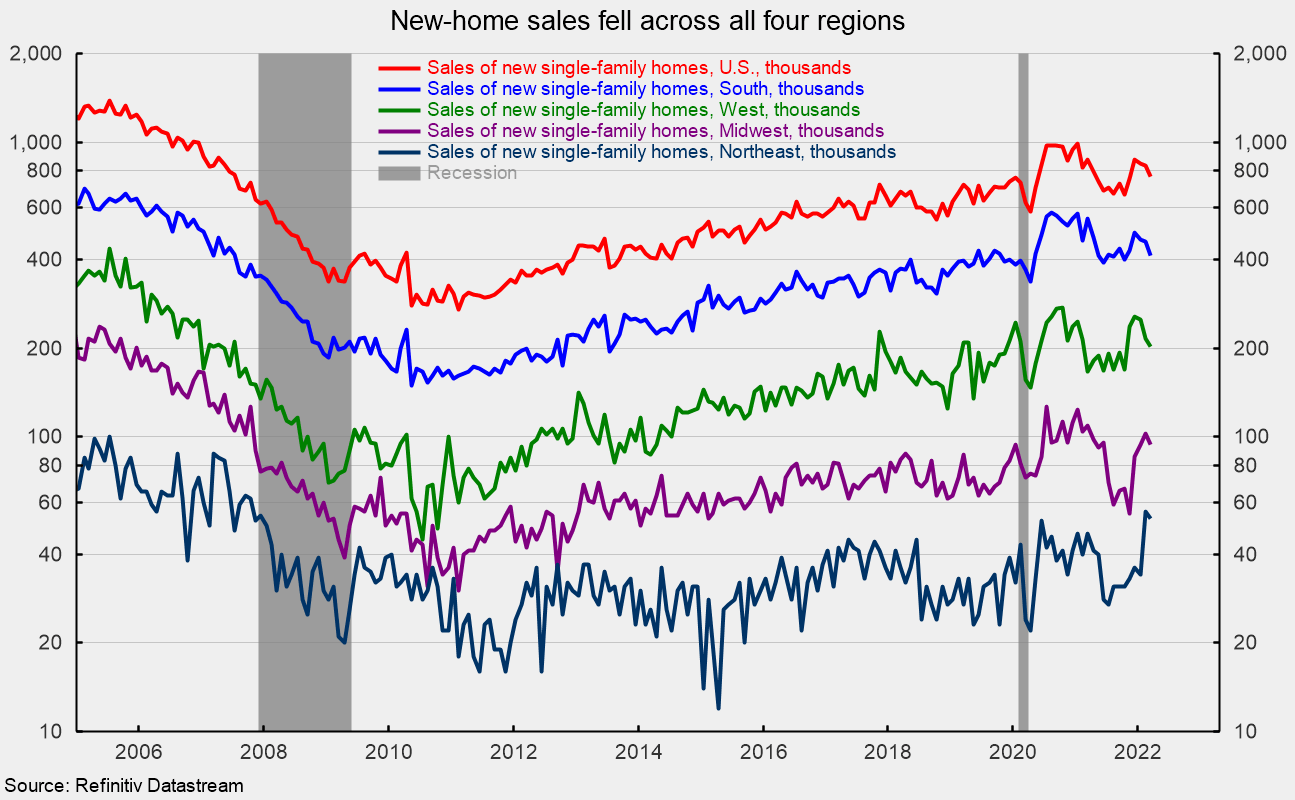

Gross sales of latest single-family houses have been down in all 4 areas of the nation in March. Gross sales within the South, the biggest by quantity, fell 10.2 % whereas gross sales within the West dropped 6.0 %, gross sales within the Midwest decreased 8.7 % and gross sales within the Northeast, the smallest area by quantity, sank 5.4 % for the month. From a yr in the past, gross sales have been up 12.8 % within the Northeast and up 21.0 % within the West, however are off 13.8 % within the Midwest and off 24.7 % within the South (see second chart).

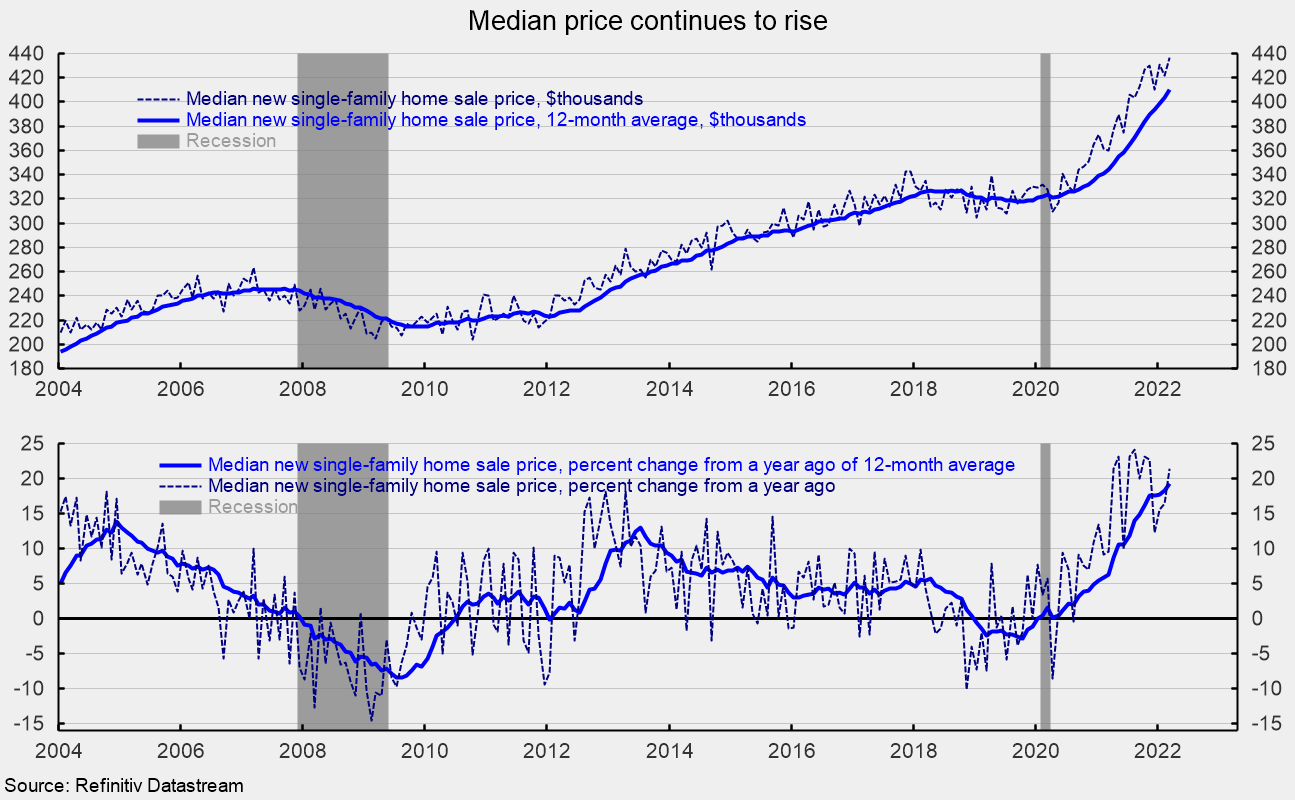

The median gross sales worth of a brand new single-family residence was $436,700 (see prime of third chart), up from $421,600 in February (not seasonally adjusted). The achieve from a yr in the past is 21.4 % versus a 16.5 % 12-month achieve in February (see backside of third chart). On a 12-month common foundation, the median single-family residence worth remains to be at a report excessive (see prime of third chart) whereas the achieve from a yr in the past within the 12-month common is nineteen.3 % (see backside of third chart).

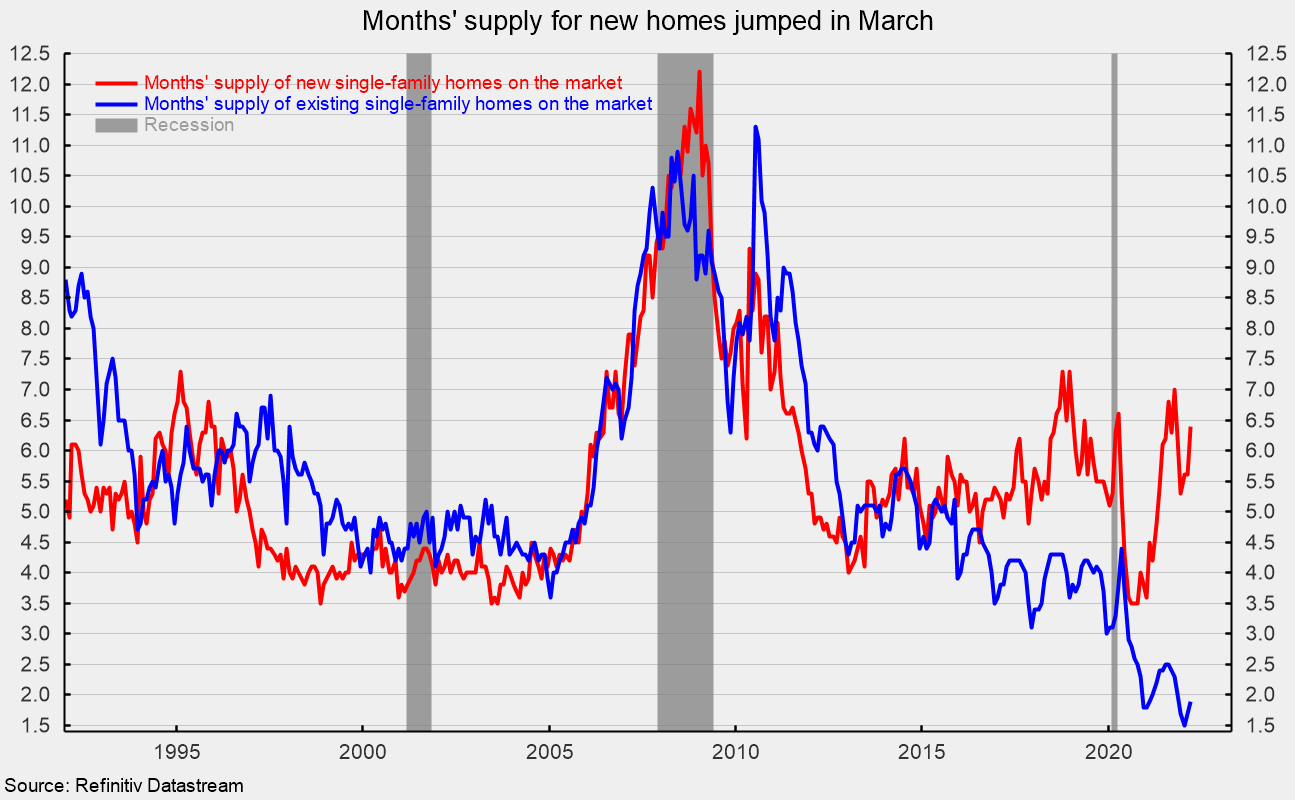

The overall stock of latest single-family houses on the market rose 3.8 % to 407,000 in March, placing the months’ provide (stock instances 12 divided by the annual promoting charge) at 6.4, up 14.3 % from February and 52.4 % above the year-ago stage (see fourth chart). The months’ provide is at a comparatively excessive stage by historic comparability and is considerably greater than the months’ provide of present single-family houses on the market (see fourth chart). The comparatively excessive months’ provide and surge in mortgage charges could also be among the many causes for slowing positive aspects within the median residence worth. The median time available on the market for a brand new residence remained very low in March, coming in at 3.0 months versus 2.9 in February.

Robert Hughes

Robert Hughes joined AIER in 2013 following greater than 25 years in financial and monetary markets analysis on Wall Avenue. Bob was previously the top of World Fairness Technique for Brown Brothers Harriman, the place he developed fairness funding technique combining top-down macro evaluation with bottom-up fundamentals.

Previous to BBH, Bob was a Senior Fairness Strategist for State Avenue World Markets, Senior Financial Strategist with Prudential Fairness Group and Senior Economist and Monetary Markets Analyst for Citicorp Funding Companies. Bob has a MA in economics from Fordham College and a BS in enterprise from Lehigh College.