{kind=link}

I’ve cash however I’m scared to take a position now in equities…

Most of us throughout our working careers could have two types of money flows

- Common Money Inflows from Month-to-month Wage

- Occasional Money Inflows – bought a property, efficiency bonus, bought esops, inheritance and so forth

In terms of common money inflows, SIP (Systematic Funding Plan) is an easy and confirmed long-term method to take a position and develop your month-to-month financial savings. This works completely properly for many of us and in addition automates the complete decision-making course of.

Nevertheless, the choice to take a position occasional money flows into equities shouldn’t be so easy and will get just a little daunting, particularly, when the quantity is massive.

The largest fear level is the inevitable query – “Is now the suitable time?”

- Must you make investments now or anticipate a market correction?

- What when you make investments now and the market falls?

- What when you don’t make investments now and the market continues to rally?

- What if markets right and you aren’t in a position to enter again on the proper time?

Now allow us to be trustworthy. Considering via these questions is advanced, troublesome, and takes quite a lot of psychological effort. We frequently get into the ‘analysis-paralysis’ mode.

Ultimately, most of us find yourself selecting the simplest selection – ‘I WILL DECIDE LATER’.

What when you had a easy framework that might information you thru this choice, not solely now but in addition within the years to come back.

That is precisely what we can be sharing with you on this article.

Have a sip of excellent chai and allow us to dive in…

What’s the generally prescribed resolution when you must make investments a big sum of cash into equities?

The frequent knowledge goes like this…

“The very best time to spend money on equities is the time when you have got the cash”

Whereas there’s a pure tendency to dismiss this steerage on the premise of its simplicity, let’s verify for precise proof and discover out if this rule stands the check of time.

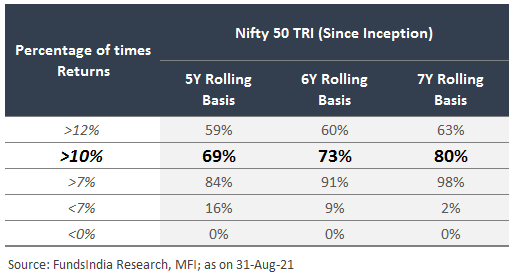

Any investor who invests in Fairness markets is mostly anticipated to have at the least a 5-7 12 months time-frame. Allow us to verify your odds of constructing respectable returns over a 5Y-7Y interval masking each potential funding date within the final 22+ years.

GREAT!

Roughly 70% of the time, a easy ‘invest-immediately-when-you-have-the-money’ technique mixed with a great deal of persistence to disregard frequent market tantrums supplied you respectable return outcomes (better than 10% CAGR) over 5 years. Additional, merely extending time frames by 1-2 years improved the chances to round ~80%.

So, the easy rule – “The very best time to spend money on equities is the time when you have got the cash” is sensible and works properly 80% of the time.

BUT…

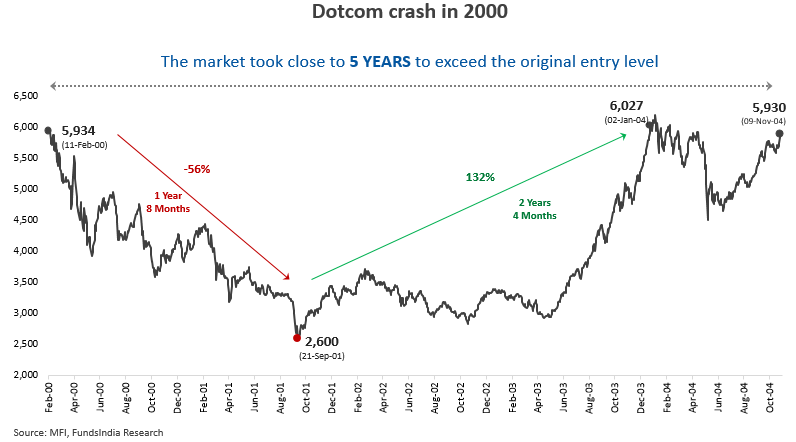

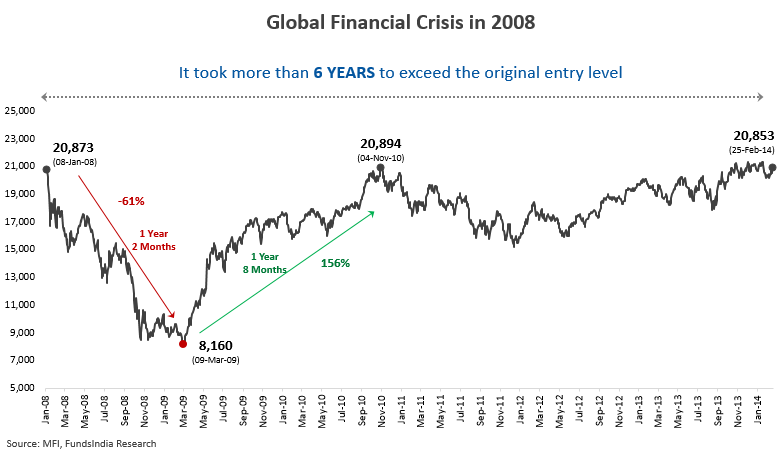

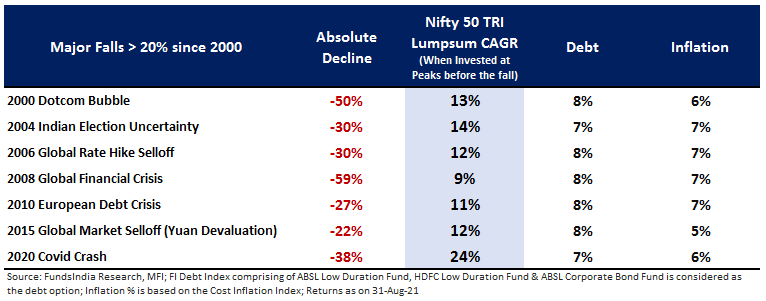

What if we find yourself within the unfortunate 10-20% a part of the statistics the place even the 5-7 12 months returns seemed dismal?

To place that in perspective, that is how dangerous it will get if you get the entry fallacious…

Whereas this will look scary, even investing on the worst entry level labored out properly if given extra time and persistence (however lots increased than what’s often required).

So does it imply the answer is – to take a position when you have got the cash?

Whereas this resolution works completely properly over lengthy durations of time, there’s a small nuance that it ignores – the easy incontrovertible fact that – You and I are HUMAN!

It’s a lot simpler to investigate these long-term returns in hindsight. However sadly, this evaluation ignores a very powerful issue which can’t be backtested – YOUR EMOTIONS.

The sensation of remorse and sleepless nights, if you make investments your cash and it begins to go down instantly, can’t be totally understood till you have got skilled it.

Think about residing with the frustration of ‘If solely I had waited for some extra time’, for a number of years.

- The extra this painful interval prolongs, increased the chances of you and I giving up on our investments (learn as promoting and taking out our cash at a loss).

- Bigger the sum of cash, the better the emotional ache and better the probabilities of giving up.

So whereas theoretically, shopping for each time you have got the cash is an honest method, in actuality, the easy incontrovertible fact that we’re emotional and human, implies that that is far simpler stated than completed.

Now how can we clear up this?

The place to begin is to just accept that the BEST technique to deploy your cash will solely be recognized 5 years later. Proper now, we’re coping with a number of variations of the long run that may presumably play out.

Clearly, in hindsight, it will likely be crystal clear on which technique was the most effective as just one model of the long run would have performed out.

Since we are able to’t predict which model of the long run will play out, the fundamental thought is to optimize for a technique that may allow you to decrease remorse throughout completely different variations of the long run which may play out.

However what does this actually imply?

Allow us to begin from the fundamentals.

Within the close to time period (say subsequent 1 12 months), markets can have three completely different variations of the long run

Model 1: Market strikes up

Model 2: Market goes down

Model 3: Market stays flat

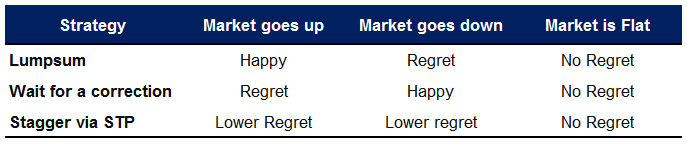

Allow us to begin with the only two choices to deploy our cash:

- Do a lump sum (i.e make investments the complete cash at one go)

- Await a correction to take a position

Now since we don’t know whether or not markets will go up or down within the close to time period, each decisions have one state of affairs the place we’ll remorse.

Whereas it’s not potential to get rid of remorse utterly, what if we mix each methods to try to decrease the remorse.

In different phrases, as a substitute of placing the complete cash at one go, we unfold it throughout an extended time-frame. This may be completed through the STP (Systematic Switch Plan) choice the place we first park the complete cash in a secure debt fund and switch it to the meant fairness fund at predefined intervals (say weekly or month-to-month) over a specified time-frame.

On this case,

- If markets go up…

Had you waited for a market correction you’ll have regretted lacking the complete rally. Now your remorse is decrease as you’re already partially invested and proceed to take a position. - If markets go down…

Had you invested every little thing at one go you’ll have regretted your choice as your complete cash is down. Now your remorse is decrease as you didn’t make investments every little thing at one go and just some quantity is invested. Additional you additionally get to take a position the remainder of the cash at decrease costs.

However now comes the following logical query…

How lengthy do you stagger?

State of affairs 1: In the event you stagger over a very long time body and the market instantly strikes up you continue to have a big a part of your cash not collaborating within the fairness rally.

State of affairs 2: In the event you stagger over a short while body and the market goes down you continue to have a big a part of your cash taking a success within the fairness fall.

So we’d like a framework to cut back our remorse even whereas we stagger our cash

Right here is how we’re considering via this dilemma…

Rule 1: Bigger the Quantity, Longer the Deployment Time

The bigger the amount of cash the extra we fear concerning the draw back in comparison with the upside. Your means to deal with the identical 20% fall is perhaps very completely different relying on whether or not you have got Rs 10 lakhs or Rs 10 crores to take a position.

Behavioral Science additionally helps this view and has discovered that the ache of dropping is extra acute than the pleasure of achieve – we really feel nearly twice the emotion over a loss versus a achieve. That is known as Loss Aversion.

One solution to clear up that is utilizing a easy rule – Bigger the Quantity, Longer the Deployment Time

However what’s a big quantity for me is perhaps a small quantity for another person. How can we contextualize this?

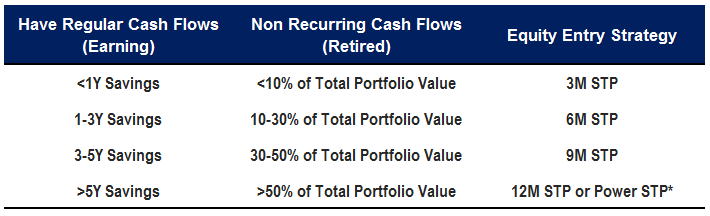

Right here is how you are able to do this for the 2 broad classes of buyers

- Retired with no future money flows

- On this case, the brand new quantity as a % of the present portfolio may help you contextualize the relative worth

- Incomes with common money flows

- On this case, the brand new quantity represented as ‘no of years it takes to avoid wasting this quantity’ may help contextualize the relative worth

Primarily based on the above thought course of, allow us to construct our entry technique:

*The FundsIndia Energy STP is a completely automated, clever valuation-driven deployment technique that helps you make investments massive lump sum quantities into equities anytime with out worrying about present market valuations. You’ll be able to learn extra about this right here.

Whereas this can be a ok method, how can we enhance this additional?

Enter Valuations!

Rule 2: Extra Costly the Valuation, Longer the Deployment Time

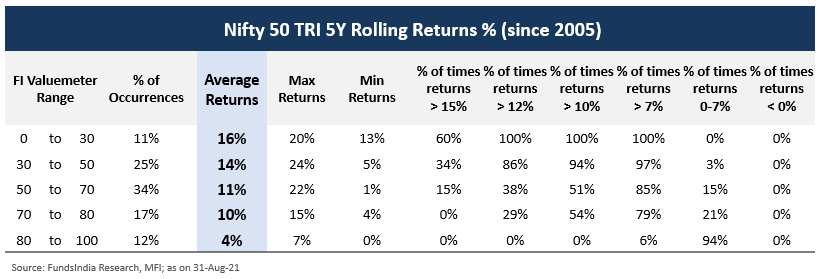

After we studied previous Indian market historical past, we discovered that valuations are often inversely correlated to long run fairness returns (i.e increased beginning valuations point out increased odds of decrease long run fairness returns and vice versa)

We went again 16+ years and checked for future 5-year fairness returns for Nifty 50 TRI at completely different beginning valuations (proxied by our inner valuation indicator – FundsIndia Valuemeter – based mostly on 4 valuation parameters – MCAP/GDP, PE Ratio, PB Ratio and Earnings Yield/GSec Yield).

Here’s what we discovered…

Takeaway:

- Dearer the beginning valuation, increased the chances of dismal future returns – higher to deploy slowly over an extended time period

- Decrease the beginning valuation, increased the chances of excellent future returns – higher to deploy instantly over shorter time frames

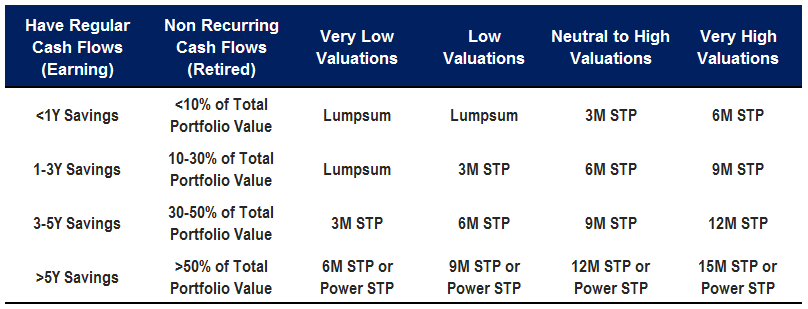

Including Valuations to our preliminary framework, and mixing each Rule 1 and Rule 2

Framework for Deploying New Cash into Equities

**In case you are utilizing our FundsIndia Valuemeter, right here is how one can apply them to completely different valuation zones

Very Low valuations: 0-30, Low Valuations: 30-50, Impartial to Excessive Valuations: 50-80, Very Excessive Valuations: >80

As we emphasised earlier, please keep in mind that this framework doesn’t assure you the very best entry level (as this may solely be recognized in hindsight relying on whether or not the market strikes up or down and for a way lengthy).

This framework’s main intent is that will help you handle the problem of choice paralysis, particularly when coping with massive quantities and an unsure close to time period (which is sort of at all times the case).

Its important job is that will help you decrease your future remorse throughout completely different potential near-term outcomes (market going up or down) and offer you peace of thoughts with out too many “what ifs” to fret about.

Summing it up

- I’ve cash however I’m scared to take a position now in equities?

- Must you make investments now or anticipate a market correction?

- What when you make investments now and the market falls?

- What when you don’t make investments now and the market continues to rally?

- What if markets right and you aren’t in a position to enter again on the proper time?

- Evaluation Paralysis resulting in frequent response – ‘I’ll determine later’

- Make investments when you have got the cash – Proper method however behaviorally very troublesome to implement

- Whereas REGRET can’t be eradicated utterly, it may possibly minimized

- Rule 1: Bigger the Quantity, Longer the Deployment Time

- How one can determine what’s a ‘massive’ quantity?

- Retired with no future money flows – New quantity as a % of the present portfolio

- Incomes with common money flows – New quantity represented as ‘no of years it takes to avoid wasting this quantity’

- How one can determine what’s a ‘massive’ quantity?

- Rule 2: Extra Costly the Valuation, Longer the Deployment Time

- Construct an Entry Framework combining Rule 1 and Rule 2 to attenuate remorse and keep away from choice paralysis

Different articles chances are you’ll like

Put up Views:

13,532