{kind=link}

Asset Allocation refers to the way you break up your cash throughout totally different belongings reminiscent of Fairness, Debt, Gold and so on.

This deceptively easy determination might be the only most essential determination in terms of investing your cash.

Tutorial analysis demonstrates that roughly 80-90% of your long-term funding returns and funding expertise may be traced again to your asset allocation determination.

The misleading simplicity of the choice, nevertheless, typically results in underappreciation of its effectiveness.

Given the numerous significance of this determination, here’s a framework that can assist you make a wise and knowledgeable asset allocation selection.

The Regular Strategy

Often when you find yourself requested to resolve in your asset allocation, you might be proven some variation of 4-5 asset allocation fashions with fancy names reminiscent of conservative, average, aggressive and so on. All these fashions will often have various levels of fairness publicity with the broad assumption – larger the fairness publicity larger the danger/returns and vice versa.

Here’s a tough model:

- Danger Stage 1: 10% Fairness: 90% Debt

- Danger Stage 2: 30% Fairness: 70% Debt

- Danger Stage 3: 50% Fairness: 50% Debt

- Danger Stage 4: 70% Fairness: 30% Debt

- Danger Stage 5: 90% Fairness: 10% Debt

Now allow us to assume you’ve gotten Rs 1 cr to speculate and a ten yr time-frame. We are going to now venture the long run potential worth of your portfolio primarily based on anticipated returns from fairness and debt and ask you to decide on what you need.

For eg allow us to assume 12-14% return expectation for Fairness and 5-7% for Debt over the subsequent 10 years. (you possibly can plug in your assumptions)

- 10% Fairness & 90% Debt: 5-7% return expectation i.e ~ Rs 1.65 crs to 2 crs after 10 years

- 30% Fairness & 70% Debt: 7-9% return expectation i.e ~ Rs 2 crs to 2.4 crs after 10 years

- 50% Fairness & 50% Debt: Sept. 11% return expectation i.e ~ Rs 2.4 crs to three crs after 10 years

- 70% Fairness: 30% Debt: 11-13% return expectation i.e ~Rs 3 crs to three.6 crs after 10 years

- 90% Fairness: 10% Debt: 12-14% return expectation i.e ~ Rs 3.3 crs to 4 crs after 10 years

Now what is going to you decide?

Clearly, the upper return model!

Give it some thought this fashion. If you’re coming for a weight reduction programme and I ask you – Do you wish to lose 3 kgs or 5 kgs or 10 kgs or 15 kgs?

What’s going to you reply?

After all, 15 kgs!

The catch right here is that we’re being bought solely on outcomes.

That is completely superb from a marketer’s viewpoint, who will vouch for the cardinal rule – ‘By no means promote the method however promote the end result’.

However the actual downside lies right here. Typically we neglect that there’s a corresponding effort required from our facet. Larger weight reduction may also imply we have to put much more effort – reducing junk meals, consuming veggies, common exercises, higher sleep and so on.

Most of us acknowledge this ‘larger effort’ half in terms of health. However in terms of investing, we conveniently neglect this!

In investing, we take the outcomes as a right. It’s assumed that if you happen to keep long run and put up with volatility you get the returns. The phrase “volatility” sadly is a little bit imprecise and understates the precise emotional ache and uncertainty that we have to undergo.

Outcomes, little question, are a neater solution to make you purchase. Nonetheless, understanding the precise journey and emotional ache that you’ll have to undergo after which deciding on an asset allocation plan will make sure you stick on with the plan and realise the meant final result!

What if we flipped the method and began with serving to you perceive the journey first and final result later.

Enter the TTT Framework

The TTT Framework consists of three components –

- Time Body

- Tolerance to Declines

- Tradeoff

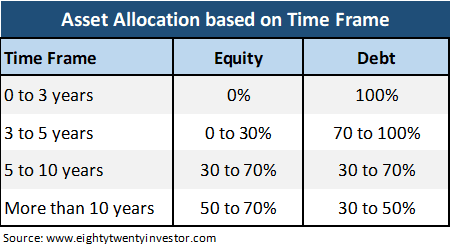

1. Time Body

The very first thing you’ll want to know is your approximate funding time-frame.

The logic is straightforward:

- Debt returns whereas they supply comparatively decrease returns over the long term, they’re secure and constant over the quick time period.

- Fairness returns whereas they’ve the potential to offer larger long run returns, in shorter time frames their returns may be a lot decrease than debt fund returns and even detrimental.

In order time frames improve you possibly can have larger allocation to fairness.

Why haven’t we included something above 70% Fairness Allocation?

Over time, after coping with a number of purchasers, we’ve realized that 80-100% fairness allocation is extraordinarily troublesome to drag off for many of us. Except you’ve gotten skilled 2 market cycles and are pretty palms on with fairness investing, we might counsel no less than 30% in debt allocation.

Additionally when examined over the past 30 years, in the long term, a 70% Fairness:30% Debt portfolio with yearly rebalancing, supplies returns which is fairly near a pure 100% fairness allocation with far decrease intermittent non permanent declines.

In our instance, you’ve gotten a time-frame of round 10 years and therefore allow us to go by the bucket 5-10 years. This suggests an allocation between 30% to 70% in Equities.

Now how do you resolve whether or not it’s 30% or 40% or 50% or 60% or 70% in Equities?

Phew! Too many selections and this may increasingly paralyze your determination making.

So allow us to simplify our option to 30%, 50% and 70%.

2. Tolerance to Momentary Declines

Don’t get delay by the flamboyant jargon. In easy phrases, the query you’ll want to reply is “What extent of non permanent portfolio falls will you be comfortable with?”

Whereas long run is okay, in actual life most of us consider our portfolios within the quick time period. So except you’ve gotten a clear understanding of what’s okay and what’s not okay within the quick time period, long run returns will stay solely on paper as you could panic out on the first signal of a market fall.

However what is brief time period?

Behavioral Scientists ask us to not monitor our portfolio too regularly because it results in larger odds of seeing detrimental returns and excessive risk of a knee jerk response.

Whereas 1 yr monitoring interval would have been excellent, sadly, this can be a tall ask as most of us discover it to be too lengthy. 3 months which is when most evaluations are accomplished is simply too frequent.

We predict the candy spot for portfolio analysis is 6 months.

You can begin evaluating portfolios in 6 month blocks. For eg, a ten yr interval, as a substitute of being considered as one long run interval can as a substitute be considered as a mixture of 20 discrete 6 month quick time period durations.

Now all of us know that fairness markets undergo lots of non permanent declines.

However, what diploma of MARKET FALL is meant to be NORMAL?

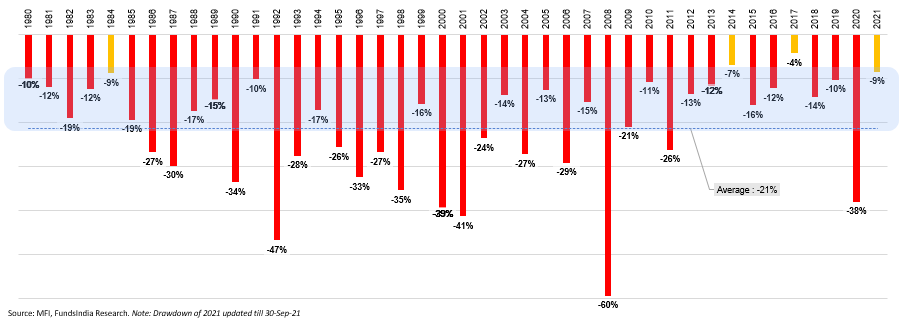

The best solution to perceive that is to seek advice from the previous conduct of fairness markets.

So, we went again so long as 40+ years (from the time Sensex was launched) and determined to verify for the largest fall recorded throughout annually i.e the autumn from the best index worth to the bottom index worth throughout a yr.

Here’s what we discovered…

- Fairness markets had a brief fall EACH & EVERY YEAR! In truth, there was not a single yr the place the markets didn’t have a brief decline.

- A ten-20% non permanent fall was virtually a given yearly.

- There have been solely 3 out of 41 years (represented by the yellow bars) the place the intra-year fall was lower than 10%.

So when you have a 100% fairness portfolio, a 10-20% non permanent fall must be anticipated virtually yearly.

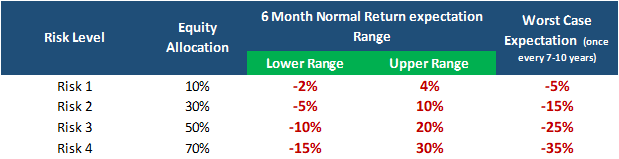

We additionally did the same evaluation for various asset allocation ranges and right here is the way it roughly seems to be

The above desk offers you a tough vary of returns that will be thought-about to be regular (taking the previous as a information) for various asset allocation portfolios.

For instance, when you have a 70% fairness allocation, 95% of the occasions you possibly can anticipate your portfolio returns to be wherever between -15% to 30% over the subsequent 6 month interval. You too can see that as you attempt to cut back your detrimental return vary, you additionally find yourself reducing your upside as properly.

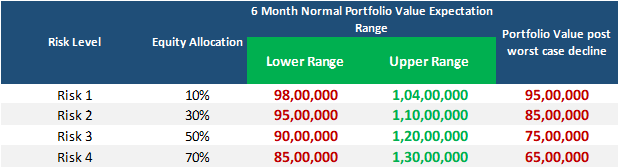

To make this complete train extra significant and actual, allow us to convert this % into Rs phrases..

Now for the portfolio of Rs 1 cr, allow us to assume you’ve gotten chosen Danger 4 (70% Fairness: 30% Debt).

What must be your expectation from this asset allocation selection?

- A return vary of -15% to 30% within the subsequent 6 months must be thought-about as regular i.e your portfolio may be wherever within the vary of Rs 85 lakhs to 1.3 crs.

- In different phrases, for a brief fall of upto Rs 15 lakhs in your portfolio, you might be anticipated to say “Nothing to fret. That is precisely what I signed up for and the portfolio is behaving as per my expectations!”

For those who observed, I had stealthily used the phrase “regular”. For those who thought a 15% non permanent fall is all that you must tolerate for a Danger 4 asset allocation, dangle on.

Right here comes the killer.

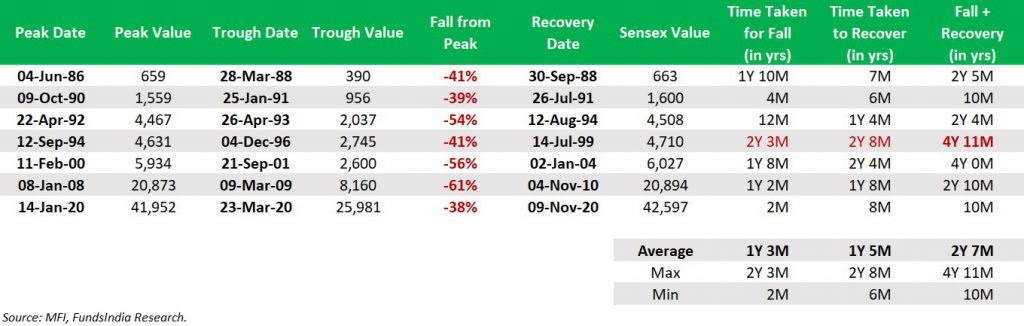

Often, there are additionally excessive non permanent falls (learn as bear markets) in equities of greater than 30%. This will grow to be as unhealthy as 40-60% decline (as seen in the course of the 2020, 2008 and 2000 market crash). Whereas they don’t essentially observe any sample and may occur anytime, traditionally they’ve occurred as soon as each 7-10 years. Whereas we’ve no clue when or what is going to result in the subsequent bear market, we may be fairly positive that we are going to positively see lots of bear markets over our investing lifetimes.

After going by 40 years of Sensex historical past, the best fairness fall has been round 40-60% (within the 2020, 2008 & 2000 crash). In order part of our expectations we should even be comfortable with struggling a big crash as soon as each 7-10 years.

The extent of the big however non permanent decline will rely upon the fairness allocation as proven beneath (assuming a 50% decline).

So if you happen to select Danger 4 portfolio, over the subsequent 7-10 years, it’s extremely probably that your portfolio can quickly go down upto 35% someday over the subsequent 10 years.

Percentages make it rather less scary. Let me confront you with actuality…

For those who select the Danger 4 portfolio and there’s a massive crash within the subsequent 6 months, your portfolio can quickly go down upto Rs 65 lakhs.

Would this be comfortable with you?

Like I imply, severely, assume by these values and what it could imply to you.

At this juncture, you possibly can resolve to scale back your anticipated declines and make your funding journey much less painful by shifting to Danger Stage 3 or Danger Stage 2.

Allow us to assume you’ve gotten moved all the way down to Danger 3 (i.e 50% Fairness Allocation).

This may grow to be our new expectation…

- You might be comfy with a return vary of -10% to twenty%, over the subsequent 6 months and can contemplate this as regular conduct from the portfolio.

- This interprets to a price between Rs 90 lakhs to Rs 1.2 crs.

- Additionally within the worst case, you might be mentally okay placing up with a brief decline of 25% or Rs 25 lakhs.

Now you’ve gotten a tough estimate of your asset allocation. Allow us to transfer to the ultimate step.

3. Commerce-off between lowering quick time period declines and long run returns

As with all the pieces in life, reducing the anticipated declines within the quick time period comes with a long run commerce off – LOWER RETURNS!

Allow us to put some tough numbers to see what we stand to lose in the long run for a extra comfy quick time period. Assume that you just anticipate 12% returns from equities and 6% from debt (you possibly can plug in your personal numbers primarily based in your future return expectations).

Allow us to see that as precise nos…

Ah! Now it turns into clear. Our transfer from Danger 4 to Danger 3 might value us roughly round Rs 50 lakhs sooner or later. However that’s superb. That is the associated fee for lowering our nervousness and sleeping properly.

There isn’t any proper or improper reply.

The straightforward thought is to assume by the tradeoffs between quick time period ache and long run returns and decide an allocation which fits you.

Whereas shifting again to Danger 4 may appear tempting, the hot button is that you’ll want to actually introspect if it is possible for you to to remain by the journey to benefit from the final result. This can be the “paleo eating regimen” model of the funding portfolio for you. Good outcomes however rattling robust to observe over the long term.

We hope you bought the gist. That is how one can resolve on a wise and sensible asset allocation selection.

Placing all of it collectively

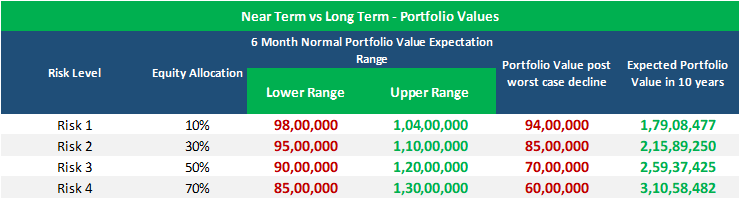

So right here is how your allocation seems to be

Cash you wish to make investments: Rs 1 cr

Lengthy Time period Asset Allocation: Danger Stage 3 – Fairness 50% + Debt 50%

Expectation (to be revised each 6 months in 1st week of January and July)

- Subsequent 6 month Return Vary which can be thought-about as regular conduct out of your portfolio: -10% to +20% i.e the portfolio worth may be wherever between Rs 90 lakhs to 1.2 crs over the subsequent 6 months

- Worst Case Expectation: -25% decline i.e the portfolio worth may be quickly all the way down to Rs 75 lakhs.

Lengthy Time period Return Expectation: ~Rs 2.4 crs in 10 years and return expectation round 9% (primarily based on assumptions Fairness:12% and Debt:6%)*

Actuality Verify…

Whilst you have chosen your allocation. Let me additionally remind you of some different realities.

Throughout such falls, often it takes round 1-3 years to get again to unique ranges and for your complete interval, your portfolio returns might look dismal. Ideas of “I ought to have merely caught to FD”, “Have I accomplished the improper factor” and so on will hang-out you and take a look at your religion within the asset allocation that you’ve chosen. A number of specialists will name for shifting from fairness to debt or money until there’s readability, and can additional add gas to your uncertainty and doubt. Because the market falls, you’ll look extra silly with every passing day. Your hard-earned cash will hold taking place day-after-day.

Now it’s not possible so that you can think about how this actually feels and predict whether or not you’ll actually be capable to pull this off. Your previous conduct in bear markets is the closest you will get to grasp your tolerance to draw back.

What did you do in Feb-Mar 2020 when the fairness markets fell by ~38%?

- For those who bought your complete fairness allocation: Chances are you’ll be overestimating your tolerance ranges. On this case stick near the decrease band of 30% Equities.

- For those who bought part of your fairness allocation: On this case, don’t exceed 50% fairness allocation.

- Held Regular or Purchased extra: Your chosen asset allocation is nice to go!

Summing it up

Our TTT Framework

- Time Body

- Larger the timeframe larger the fairness allocation

- No more than 70% Fairness Allocation

- Tolerance for Declines

- Anticipated Regular Declines

- Anticipated Worst Case Declines

- Verify in precise values and never percentages

- Tradeoff between threat and returns

- Perceive the long run commerce off in returns

You will have your Asset Allocation prepared.

With this single determination you’ve got 80% of your funding plan sorted!

From this level on, the one factor left to do is to stay to the deliberate asset allocation and rebalance as soon as yearly if there’s a deviation over +/-5%.

Until the subsequent time, blissful investing as at all times 🙂

Different articles you could like

Submit Views:

9,409