{kind=link}

Yesterday’s publish analyzed the drivers of the surge in inflation over the course of 2021 by means of the lens of the New York Fed DSGE mannequin. In immediately’s publish, we use the mannequin to review how different financial coverage methods may contribute to bringing inflation again all the way down to 2 %. Our most important discovering is that there isn’t any financial silver bullet. Because of a flat Phillips curve—a nicely–documented characteristic of the financial setting of the final three a long time—financial coverage can solely obtain sooner disinflation at a substantial price by way of forgone financial exercise. That is true whatever the systematic method adopted by the central financial institution within the mannequin to pursue its goal.

Financial Coverage and Value-Push Shocks

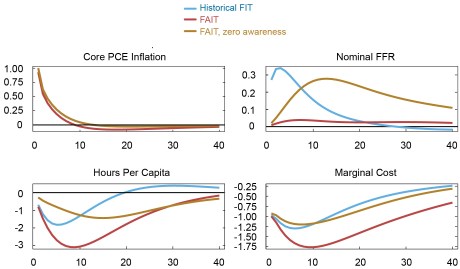

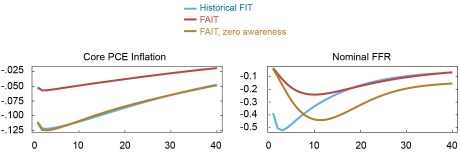

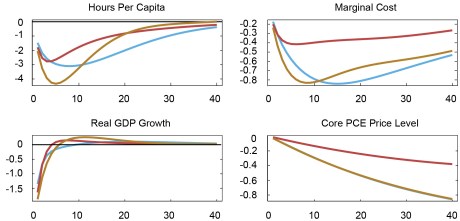

Yesterday’s publish highlighted that inflation is at present elevated on account of cost-push shocks. How does the mannequin economic system reply to such shocks? And the way does this response change with totally different financial coverage response capabilities? The chart beneath solutions these questions. It reveals how a number of macroeconomic variables reply to a cost-push shock of the identical measurement as that estimated to have hit the U.S. economic system within the second quarter of 2021. A shock of this measurement results in a shock improve in inflation of roughly 1 %. This impression impact is decrease than the general improve in inflation in that quarter as a result of cost-push shocks in that quarter are probably the most outstanding, however not the one issue behind excessive inflation. Earlier cost-push shocks, in addition to demand and different shocks hitting the economic system within the second quarter additionally contribute to the inflation improve.

As an instance how different financial coverage methods may contribute to convey inflation down, the chart consists of three traces comparable to totally different rate of interest guidelines. In blue (“Historic FIT”) is the trail of the economic system when financial coverage follows the versatile inflation-targeting rate of interest rule that was in place earlier than the summer season of 2020, as estimated by the mannequin. The purple traces present the responses below a rule that captures a number of the options of versatile common inflation concentrating on (FAIT). This rule differs from FIT primarily as a result of it responds to an common of inflation over time, somewhat than to present inflation alone. The small print of its implementation in our mannequin are described in additional element right here. We’ll talk about the gold line shortly.

The primary placing characteristic of this comparability is that the response of inflation to the cost-push shock could be very comparable whatever the coverage rule in place. The FAIT rule reduces inflation a bit sooner than the historic FIT rule, however this small profit by way of inflation management comes at a really giant actual price. The recession that financial coverage should engineer to realize this negligible discount in inflation is deeper and extra protracted below the FAIT than the FIT coverage, as judged by any of the true variables within the mannequin: hours labored, GDP development, the extent of GDP, and (actual) marginal prices. This very unfavorable sacrifice ratio displays the intense flatness of the estimated Phillips curve. FAIT “will get the job finished” with minimal actions within the coverage fee as a result of the stance of coverage is predicted to stay tight for (a lot) longer than below the estimated FIT rule. This tighter-for-longer coverage implies that the 10-year common anticipated rate of interest rises much less on impression than below FIT, however declines extra slowly. It additionally implies that the contraction in financial exercise is extra protracted, to the purpose that long-term inflation expectations truly fall, regardless of the inflationary shock. The rise in long-term nominal charges and the autumn in inflation expectations lead to a bigger improve in actual long-term charges below FAIT than below FIT, making the previous rule extra contractionary than the latter, even when it implies a smaller improve within the nominal short-term rate of interest. This explains why the recession is extra extreme, and lasts longer, below FAIT than below FIT.

Impulse Responses to a Value-Push Shock below Various Financial Coverage Methods

Within the purple impulse responses, the FAIT rule is assumed to be completely understood by non-public brokers instantly upon its adoption. However there’s some proof that expectation formation by households and corporations might regulate slowly to the introduction of the brand new coverage technique. To seize this chance, the gold traces (“FAIT, zero consciousness”) mirror the belief that personal brokers usually are not conscious of the introduction of the brand new framework and thus type expectations as if the historic FIT rule had been nonetheless in place. Each assumptions—full and partial consciousness—are excessive. Actuality might be someplace within the center, however the excessive instances assist to spotlight the significance of expectations in shaping the response of the economic system to the shock. When brokers usually are not conscious of its introduction, FAIT achieves the identical inflation end result because the historic FIT coverage, even when the coverage fee will increase rather more within the gold than within the purple simulation. It’s because, with a flat Phillips curve, the impact of present circumstances on inflation is minimal and its dynamics are largely formed by expectations. With out credibility, FAIT results in actions within the coverage fee and the true variables which can be smaller on impression than below FIT, however extra drawn out. But when this improve in persistence doesn’t alter expectations, its results on inflation are minimal.

Financial Coverage and Demand Shocks

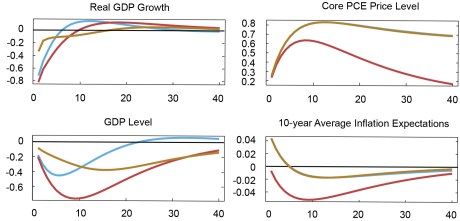

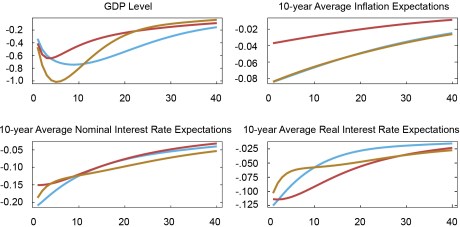

The chart above illustrates the function of other financial coverage guidelines in shaping the response of the economic system to a cost-push shock. However what if excessive inflation is because of robust mixture demand as a substitute? On this case, the inflation preventing properties of FAIT and FIT are notably totally different. That is demonstrated within the chart beneath, the place we plot the response of the identical variables thought of above to a destructive threat premium shock of the identical measurement as that confronted by the U.S. economic system within the fourth quarter of 2008, within the midst of the monetary disaster. This shock generates financial dynamics of the sort sometimes related to shifts in mixture demand, with declines in each inflation and actual exercise, as mentioned right here as an illustration. In response to a destructive threat premium shock, completely credible FAIT stabilizes inflation and the true economic system extra successfully than the historic FIT coverage, and with much less coverage effort, as measured by the actions within the nominal rate of interest. That is the textbook case in favor of insurance policies that characteristic extra historical past dependence.

Why is FAIT so profitable when confronted with demand shocks? As a result of it retains long-run inflation expectations “anchored”. As FAIT guarantees lengthy lasting lodging, 10-year inflation expectations decline by lower than half than with the FIT coverage. In flip, this suggests that the decline in long term actual charges is bigger below FAIT, even when nominal charges fall much less on impression. In flip, decrease actual charges increase demand, successfully counteracting the results of the danger premium shock. A flat Phillips curve is much less of a problem when the economic system is dealing with demand somewhat than cost-push shocks. Within the former case, the supply of the issue is a decline in mixture demand, somewhat than an exogenous improve in inflation. Due to this fact, coverage is best geared up to ship an answer by reversing the discount in demand by means of a low-for-longer technique. As well as, financial coverage is in a greater place to have an effect on financial exercise when the Phillips curve is flat, as a result of the economic system is “extra Keynesian,” as mentioned in this Liberty Avenue Economics publish. These simulations assist to know why historical past dependent insurance policies like FAIT have gained such prominence over the course of the previous twenty years, a interval by which demand shocks—together with these related to an often-binding ELB in a low r* setting—have dominated the macroeconomic panorama.

The important thing function of expectations within the success of the FAIT technique is highlighted by the truth that FIT is much less efficient at stabilizing the economic system. FIT depends much less on future guarantees and subsequently doesn’t anchor inflation expectations as a lot. For this similar cause, FAIT is much much less profitable when non-public brokers usually are not conscious of its adoption, as below the gold responses.

Impulse Responses to a Demand Shock

Conclusions and Some Caveats

This publish confirmed that, within the New York Fed DSGE mannequin, financial coverage faces an unfavorable trade-off when making an attempt to stabilize inflation in response to cost-push shocks, on account of an especially flat Phillips curve. Decreasing inflation requires a deep and protracted contraction, whatever the coverage technique underlying the pursuit of this goal. One silver lining on this pessimistic conclusion is that, if the mannequin is true and cost-push shocks are the principle cause behind inflation, their impact ought to dissipate over time, at the least based on historic patterns. If the mannequin is mistaken and inflation is pushed as a substitute by demand shocks, financial coverage is well-positioned to scale back their inflationary results.

The evaluation that results in these conclusions is topic to a number of caveats. First, brokers in our mannequin are forward-looking and perceive the construction of the economic system, together with the systematic response of financial coverage to financial developments. Because of this, the mannequin doesn’t embrace any of the mechanisms that the literature has recognized as potential sources of drift in inflation expectations. The potential for such drift may change the cost-benefit evaluation of other financial coverage approaches, as illustrated on this paper as an illustration.

Second, the Phillips curve could also be—or might have not too long ago develop into—steeper than estimated within the mannequin. Nonetheless, our calculations recommend that it might have to be even steeper than the one estimated with information as much as 1990—a interval by which the connection between inflation and actual exercise was arguably tighter than within the newer previous—for increased rates of interest to make a large dent in inflation.

Extra on the whole, the truth that a flat Phillips curve is a cause for financial coverage to be much less aggressive in stabilizing inflation, every part else being equal, is harking back to the work of Primiceri and Sargent, Williams, and Zha on the causes of the Nice Inflation of the Seventies. Of their fashions, policymakers don’t absolutely perceive the construction of the economic system and should study it as they conduct coverage. Specifically, they maintain the (mistaken) perception that the Phillips curve is flat. Because of this, they go for a much less contractionary coverage, thus feeding the upward inflation spiral. One essential distinction between our present perception that the Phillips curve is flat and that held by policymakers within the late Nineteen Sixties and early Seventies is that they weren’t but absolutely conscious of the significance of expectations within the dynamics of inflation. In distinction, the fashions used immediately to deduce the slope of the Phillips curve, together with ours, all incorporate that essential lesson from the expertise of the Seventies, even when we’ve got no assure that they achieve this accurately.

Marco Del Negro is a vp within the Financial institution’s Analysis and Statistics Group.

Aidan Gleich is a senior analysis analyst within the Financial institution’s Analysis and Statistics Group.

Shlok Goyal is a senior analysis analyst within the Financial institution’s Analysis and Statistics Group.

Alissa Johnson is a senior analysis analyst within the Financial institution’s Analysis and Statistics Group.

Andrea Tambalotti is a vp within the Financial institution’s Analysis and Statistics Group.

Disclaimer

The views expressed on this publish are these of the authors and don’t essentially mirror the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the duty of the authors.